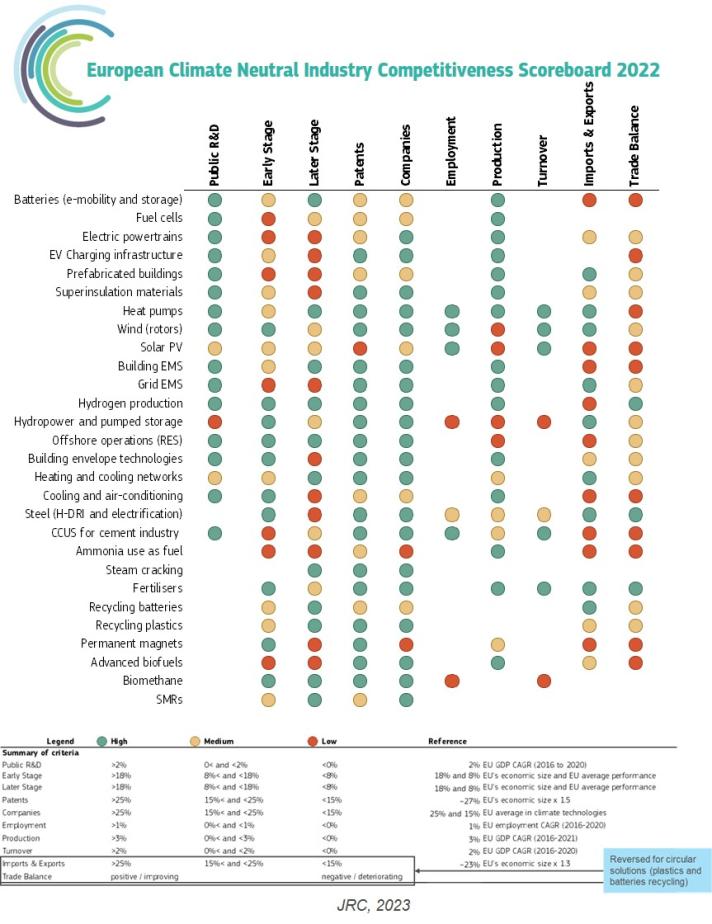

The annual assessment of key climate-neutral energy technologies finds the EU is strong in high-value patents, public R&D investment, and the number of innovating companies. The technologies in which the EU shows greatest strength are wind (rotors), heat pumps, offshore operations (for installation of renewables), and heating and cooling networks.

The results are published in the report European Climate Neutral Industry Competitiveness Scoreboard – Annual Report 2022.

It shows that EU production bounced back after the pandemic, but growing demand was increasingly met with imports. Therefore, the EU trade balance in many strategic net-zero technologies deteriorated. This indicates that EU demand for climate- neutral solutions is growing to the extent that domestic manufacturing is not able to satisfy it, and an increasing share is met with imports.

The study assesses 28 key climate-neutral energy technologies, against 10 competitiveness indicators: public R&D investment, early and late-stage venture capital investment, patent activity, number of innovating companies, employment, production, turnover, imports & exports, and trade balance.

The assessment results in a scoreboard on the technological solutions that have the potential to increase the competitiveness of European industry. This insight can help track EU’s progress toward achieving the goals of the European Green Deal and making EU climate neutral by 2050. The Gren Deal Industrial Plan introduced the Net-Zero Industry Act and the Critical Raw Materials Act to secure Europe’s lead in industrial innovation and scale up EU manufacturing of clean technologies.

The EU green technologies going strong

Among the 28 technology solutions considered, EU performs well on most indicators for wind (rotors), heat pumps, offshore operations (for installation of renewables), and heating and cooling networks.

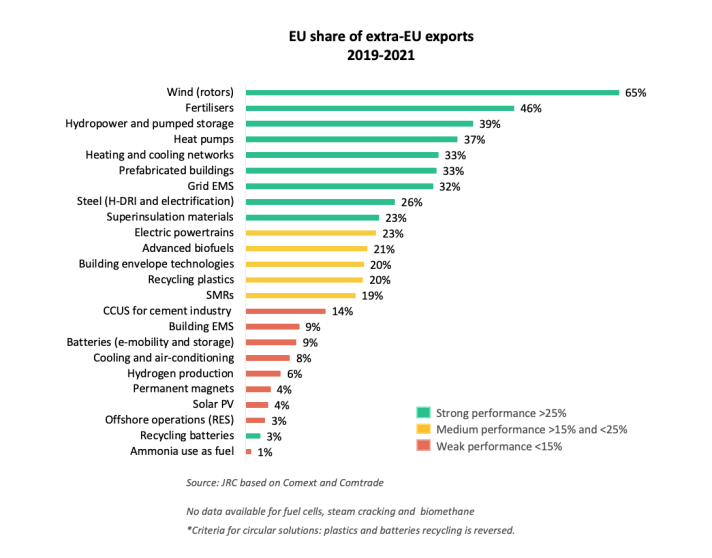

The EU leads in all innovation-related indicators for wind rotors, keeping its strong position globally with a 65% share of all extra-EU exports and hosting a substantial proportion of the global wind energy supply chain.

The heat pump industry is innovative and well placed to benefit from increasing deployment. High share of innovators is headquartered in the EU, with five corporations among the global top 10 patenting entities.

The EU hosts over 42% of all innovating companies in offshore operations, thanks to being a first mover. It has a strong production base of offshore vessels and infrastructures, and European offshore operators are well represented globally, e.g. in the Asia-Pacific region. However, rapid developments are causing bottlenecks for operators, while ports will require major upgrades to meet the offshore renewable energy targets.

The EU is a global leader in heating and cooling networks innovation. These networks play vital role in decarbonisation as about 50% of EU’s energy consumption is used for heating and cooling of buildings and industries, with 75% of this energy coming from fossil fuels. EU has a strong manufacturing capacity in the field and accounted for 33% of global exports over the period 2018-2021.

Areas of improvement

Technologies such as batteries, solar photovoltaics (PV) and hydrogen production have shown improvements.

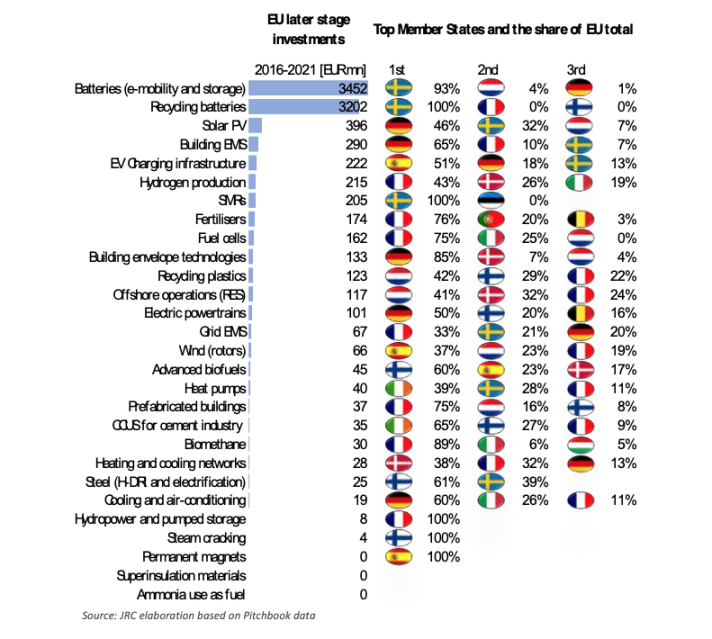

EU public R&D investment in batteries grew by nearly 40% annually in 2016-2020. Early-stage investment grew from EUR 5 million in 2010-2015 to over EUR 700 million in 2016-2021, while later stage investment increased from EUR 19 million to EUR 3.5 billion over the same period.

In solar PV, EU companies are attracting more venture capital investment than before, indicating that EU start-ups and scale-ups are becoming relatively more attractive than companies in other regions. EU production, which increased for the first time since 2016, also shows signs of revival.

As one of the main pathways for decarbonisation, the renewable hydrogen production and electrolysers sector has a high potential for growth and is attracting increasing amounts of venture capital investment. As host to 40% of global electrolyser capacity, and half of the manufacturers of large-scale electrolysers, the EU has a good industrial basis to take advantage of future market opportunities.

What are the challenges?

There are concerns for technologies linked to transport-related solutions, such as fuel cells, electric powertrains, EV charging infrastructure, ammonia as fuel, and advanced biofuels. In these, EU companies have attracted less venture capital than their global competitors. With clean mobility being one of the fastest growing sectors worldwide, there’s a risk that innovative EU companies fail to find adequate financing to scale up and relocate production to commercialise their solutions.

EU companies also capture less investment than the EU average (less than 9%) in grid energy management system (EMS) and prefabricated buildings. Both are very important, the former for enabling the functioning of smart grids and the latter for decarbonising the building sector. In another technology, building EMS, the EU trade deficit is gradually increasing, reflecting the EU’s reliance on imports when it comes to digital components and assemblies.

Another concern is the import dependency of neodymium magnets (Nd-Fe-B). These are high-performance permanent magnets indispensable for the production of wind turbines (aerogenerators) and electric vehicles (electric traction motors), as well as of a number of other advanced technologies. The EU has an increasing trade deficit, which has doubled over the last decade, reaching EUR 1 billion in 2021.

The future legislative framework, based on the European Critical Raw Materials Act, will provide incentives to increase the EU’s self-sufficiency in this domain and diversify supply. This can be reinforced by the ongoing EU R&D projects (funded by Horizon Europe), which focus on improving circularity and developing rare earth-free magnets.

Investment is largely increasing

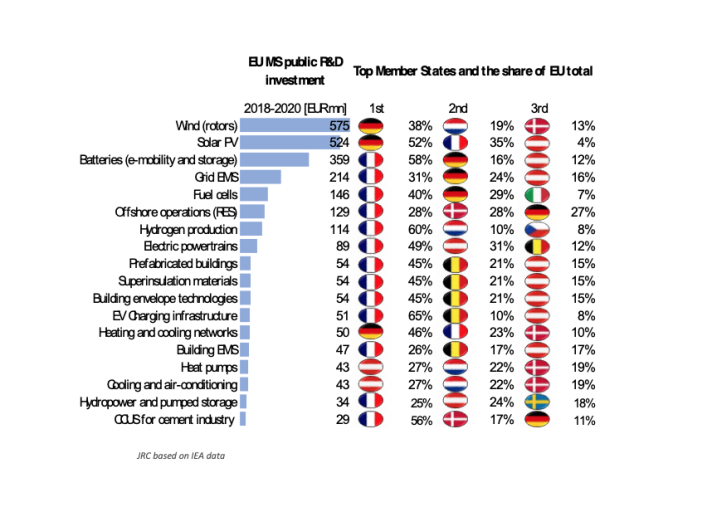

In 17 climate-neutral solutions, public R&D investment increased in the period 2016-2020. In 15 of these solutions, investment grew faster than EU GDP. From 2018 to 2020, wind and solar PV received the most public R&D investment, well above EUR 500 million.

Venture capital investment has also increased. The EU captured a higher share of later stage investment than early-stage investment in 2016-2021, though the EU still performs better at financing early ventures than scale-ups. Batteries and battery recycling concentrated almost half of EU venture capital investment in this period.

Innovation trends

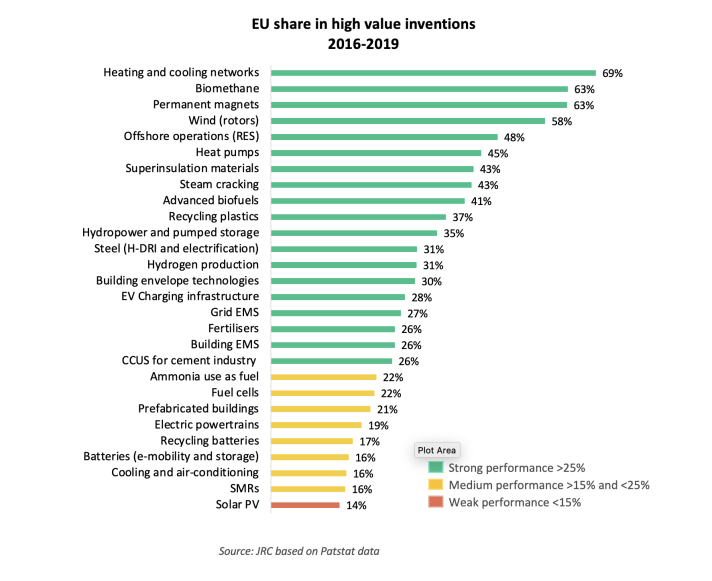

EU demonstrates strong performance in patenting activity in 19 out of 28 assessed solutions. In four solutions – heating & cooling networks, biomethane, permanent magnets and wind rotors – the EU generates over half of all high-value inventions globally. Only in solar PV, the EU performance is notably weaker, though its patent portfolio in PV is one of the largest amongst the solutions addressed.

The EU hosts over a quarter of identified innovators globally in 20 out of 28 monitored solutions. However, the EU achieves a lower performance in some key net-zero technologies like batteries and batteries recycling, fuel cells and PV.

EU trade

The EU continues to perform strongly: in 2019-2021, it accounted for over 25% of global exports in eight solutions: wind, bio-based circular fertilisers, hydropower, heat pumps, heating and cooling networks, prefabricated buildings, grid energy management system (EMS) and steel (H-DRI & electrification).

In 2021 the EU had a positive trade balance in 14 solutions and a deficit in 11. The biggest trade surpluses were in wind (EUR 2.6 billion), prefabricated buildings (EUR 1.4 billion), heating and cooling networks (EUR 1.3 billion), and grid EMS (EUR 1 billion).

The highest trade deficit was recorded in solar PV (EUR 9 billion), batteries (EUR 5 billion), cooling and air- conditioning (EUR 3 billion) and advanced biofuels (EUR 2 billion).

Background

This work contributes to the annual Clean Energy Competitiveness Progress Report, accompanying the State of the Energy Union Report, and the Clean Energy Technology Observatory and has fed insights to the Net Zero Industry Act. The solutions assessed feature in Member States’ National Climate and Energy Plans and Recovery and Resilience Plans, and are aligned with their long-term decarbonisation needs.

The technologies assessed are also aligned with REPowerEU and Net Zero Industry Act, which define the strategic net-zero technologies.

Related content

Details

- Publication date

- 15 November 2023

- Author

- Joint Research Centre