The Global Energy and Climate Outlook (GECO) 2023 presents an updated view on the implications of energy and climate policies worldwide on energy trends and emissions, and what they imply about reaching the goals of the Paris Agreement. The report provides insights into investments and related new jobs required by the transition to a low-carbon economy.

GECO 2023 - Energy, Greenhouse gas and Air pollutant emissions balances (last updated: 1 July 2024)

Projections with an energy-emissions model - using common socio-economic assumptions

GECO 2023 - Macro-economic Baseline (available soon)

Economic Multi-Regional Input-Output tables

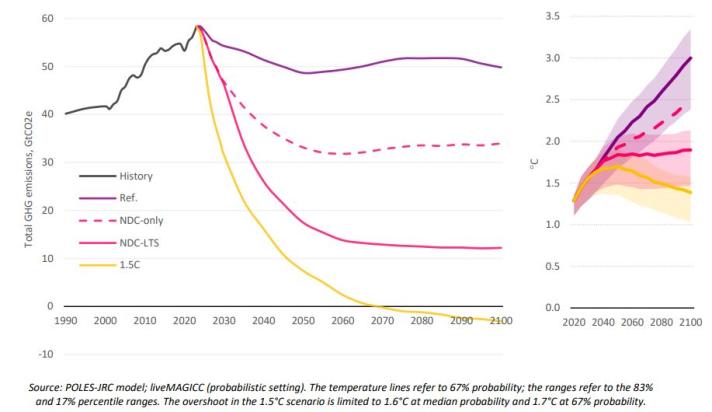

Global emissions and temperature

Global emissions projections are still not on track to deliver on the temperature targets of the Paris Agreement, but progress is being made. Policy action in major economies, continued cost reductions and accelerated deployment of low-emissions technologies in recent years lead to emissions in the Reference scenario peaking within this decade.

Both the Reference and the Nationally Determined Contribution-Long Term Strategies (NDC-LTS) scenarios fall short of limiting temperature rise to 1.5°C, with the Reference leading to a 3.0°C temperature change by 2100. Current climate policy pledges and targets in the NDC-LTS scenario imply a rapid decline in greenhouse gas emissions, but gaps remain in implementation (8 GtCO2e in 2030 compared to Reference) and in ambition (10 GtCO2e in 2050 compared to 1.5°C).

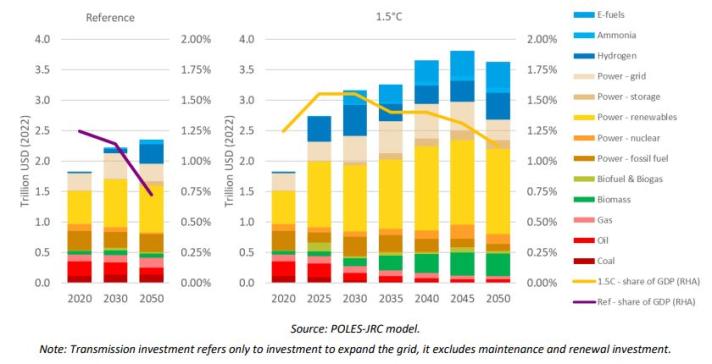

Accelerating energy-related investments

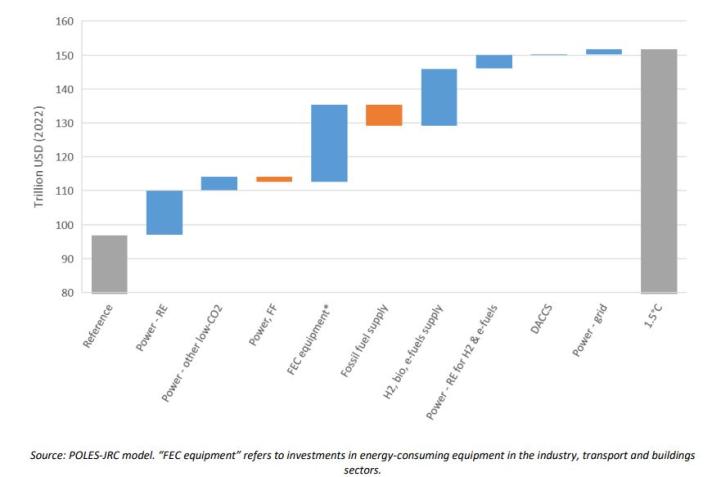

Keeping 1.5°C possible requires accelerating energy-related investments in the current decade. Annual spending on energy production and supply equipment increases by 70% in this decade compared to the previous decade, and almost doubles compared to the previous decade to reach $3.8 trillion by the middle of the century. Energy-related investment as a share of global GDP remains at the historical average of 1.4% throughout 2050, but with a particularly sharp increase in renewable power generation investment in the current decade.

Compared to the Reference scenario, significant investment in additional renewables and low-CO2 power generation happens in the 1.5°C. Higher investment needs are partly compensated by lower operating costs. Increased investment in clean energy technologies in end-use sectors such as industry, transport and buildings (e.g., electric vehicles and heat pumps) is partially offset by reduced spending on the production of fossil fuels used in power generation and end-use sectors. In the 1.5°C scenario, investments in low-emissions fuels are comparable to investments in renewables.

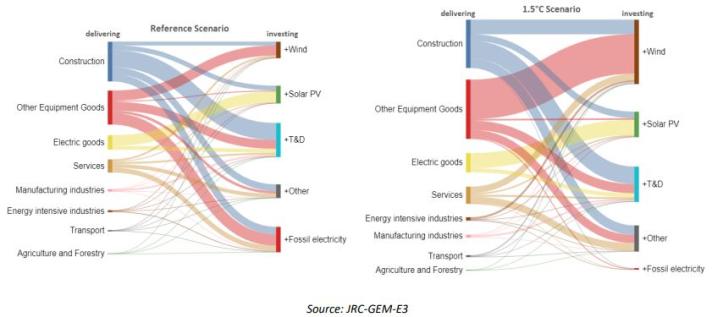

Investment spillovers and stimulus to other sectors

Compared to the Reference scenario, the additional investment in the 1.5°C scenario has knock-on effects on the investment needs of the delivering sectors. Annual investment deliveries from the construction and electronic goods sectors grow by 30%, services by 50%, and equipment goods by 80% as compared to the Reference scenario.

The higher investments in clean power technologies compensate the decline of investment deliveries to fossil fuel based power technologies, which rely primarily on the construction, equipment goods and services sectors to build additional capital stock.